Qatar’s prime minister has unintentionally fueled a family feud among the owners of German luxury sports car maker Porsche, the future of which is threatened by a takeover bid for Volkswagen.

Porsche confirmed recently that it was in exclusive talks with Qatar on investing in the heavily indebted maker of the 911 sports car.

“We are still negotiating over the share to be acquired,” Qatari Prime Minister Sheikh Hamad bin Jassem al-Thani told reporters in Doha last week, adding that a deal could be concluded within three weeks.

Qatar would like to acquire 25 percent plus one share of Porsche, a minority blocking stake that would give it a say in major decisions.

OPPOSITION

But some at Porsche, including key figures, are unhappy with that prospect, one being Ferdinand Piech, who wields considerable clout because his family is a major shareholder and he is head of the VW supervisory board.

During a meeting last week of the Porsche and Piech families, which together own Porsche, Piech expressed strong opposition to taking Qatar on as an outside investor, and was backed by his cousin, Wolfgang Porsche.

The news was reported in the media and confirmed by a source close to the matter but immediately denied by Porsche.

The company said no meeting had taken place, and that both families “unanimously support” the arrival of an outside investor.

Porsche is wholly owned by the descendants of founder Ferdinand Porsche, and while shares are traded on the stock exchange, their owners have no voting rights.

A previous attempt to open the company up to Middle Eastern investors failed.

In 1983, Piech’s brother Ernst sold his share to Kuwait, but the family immediately objected and bought the stake back, a Porsche spokesman said.

Porsche is under pressure now however because it has accumulated 9 billion euros (US$12.5 billion) in debt and needs a credit of 1.75 billion euros that the German state-owned bank KfW has resisted granting.

Porsche is not a direct victim of the economic crisis, the criteria established for access to public aid, but of its attempt to take over VW via complex stock options that backfired.

Porsche owns 51 percent of the shares in Europe’s biggest auto manufacturer.

The Porsche and Piech families appeared to have found a solution late last month when they acknowledged they could not raise their VW holding to 75 percent and agreed to a merger of the two companies.

But subsequent talks quickly broke down.

Tension is now so strong that Porsche boss Wendelin Wiedeking sent Piech a letter last month accusing Piech of harming the company’s interests with public criticism of Wiedeking, a spokesman said.

But “it’s internal opposition among the family, between Ferdinand Piech and Wolfgang Porsche,” rather than a spat between Piech and Wiedeking, an industrial source told reporters.

After Qatar sought a minority blocking stake in the German carmaker, Ferdinand Piech reportedly expressed strong opposition to the deal.

TROUBLE WITH VW

As a result, the climate has deteriorated between Porsche’s headquarters in Stuttgart, southern Germany, and VW in northern Wolfsburg. VW also did not appreciate being sidelined during the talks with Qatar.

For Porsche it is an internal matter, but “you cannot treat VW like that,” a source close to the auto giant said.

VW might decide not to extend a 700 million euro credit it has accorded Porsche.

“It is getting more and more tense,” a union source said.

Wiedeking wrote on June 9 to Berthold Huber, head of the IG Metall trade union, and threatened legal proceedings because Huber had publicly evoked “difficulties” at Porsche, spokesmen for the company and the union said.

STRONG INTEREST: Analysts have pointed to optimism in TSMC’s growth prospects in the artificial intelligence era as the cause of the rising number of shareholders The number of people holding shares of chipmaker Taiwan Semiconductor Manufacturing Co (TSMC, 台積電) hit a new high last week despite a decline in its stock price, the Taiwan Depository and Clearing Corp (TDCC, 台灣集保) said. The number of TSMC shareholders rose to 2.46 million as of Friday, up 75,536 from a week earlier, TDCC data showed. The stock price fell 1.34 percent during the same week to close at NT$1,840 (US$57.55). The decline in TSMC’s share price resulted from volatility in global tech stocks, driven by rising international crude oil prices as the war against Iran continues. Dealers said

PRICE HIKES: The war in the Middle East would not significantly disrupt supply in the short term, but semiconductor companies are facing price surges for materials Taiwan’s semiconductor companies are not facing imminent supply disruptions of essential chemicals or raw materials due to the war in the Middle East, but surges in material costs loom large, industry association SEMI Taiwan said yesterday. The association’s comments came amid growing concerns that supplies of helium and other key raw materials used in semiconductor production could become a choke point after Qatar shut down its liquefied natural gas (LNG) production and helium output earlier this month due to the conflict. Qatar is the second-largest LNG supplier in the world and accounts for about 33 percent of global helium output. Helium is

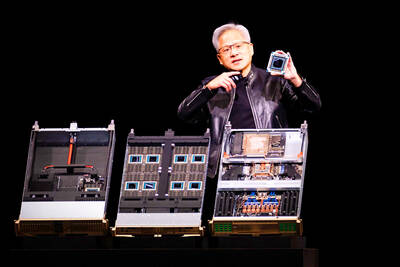

DOMESTIC COMPONENT: Huang identified several Taiwanese partners to be a key part of Nvidia’s Vera Rubin supply chain, including Asustek, Hon Hai and Wistron Nvidia Corp chief executive officer Jensen Huang (黃仁勳), addressing crowds at the company’s biggest annual event, unveiled a variety of new products while predicting that its flagship artificial intelligence (AI) processors would help generate US$1 trillion in sales through next year. During a two-and-a-half-hour keynote address, Huang announced plans to push deeper into central processing units (CPUs) — Intel Corp’s home turf — and introduced semiconductors made with technology acquired from start-up Groq Inc. The company even said it was developing chips for data centers in outer space. At the heart of Huang’s speech was the message that demand for computing power

OPTIMISTIC: Inflation still has a chance of remaining below the central bank’s 2 percent alert level, as Taiwan’s economy is resilient with healthy exports, the NDC minister said Taiwan’s inflation could exceed 2 percent this year if oil prices continue to surge amid escalating tensions in the Middle East, prompting the government to reassess its economic outlook, the Directorate-General of Budget, Accounting and Statistics (DGBAS) said yesterday. DGBAS Minister Chen Shu-tzu (陳淑姿) told lawmakers at a meeting of the legislature’s Finance Committee that the agency’s earlier growth forecast of 1.68 percent in the consumer price index (CPI) and 7.71 percent for GDP this year did not account for the ongoing Middle East conflict and would need revision, if tensions persist. The previous forecast assumed an average international crude price of